|

|||||

| New to the Plan | Actively Participating | Nearing Retirement | Enjoying Retirement | Archives | |

The Nevada Public Employees’ Deferred Compensation Program (NDC) welcomes the summer with many exciting changes and new educational opportunities to assist participants and employees with their Journey to and through retirement. Retiree Financial Wellness Fair The NDC Program held its third annual Retiree Financial Wellness Fair June 12, 14 and 15 in Las Vegas, Carson City and Sparks. The NDC Program staff and representatives from our contracted record keeper, Voya Financial®, Social Security, NVPERS, NVPEBP, Nevada Aging and Disability Services, Nevada Health Link and Morningstar® Associates were on hand to meet with current employees getting ready to retire and former government employees enjoying retirement. Each day was packed with workshops on topics retirees should consider in maintaining financial wellness in and through retirement. If you were unable to attend or view the workshops online, go to the NDC website to access this valuable information or contact the NDC Administrative Office for assistance. Governor approves Senate Bill 502 On June 1, 2017, Governor Sandoval approved Senate Bill 502, which was introduced to the Legislature bringing the Nevada Public Employees’ Deferred Compensation Program (NDC) under the direction of the Department of Administration. In a joint effort between a multitude of employee groups and the State of Nevada, the bill was amended from its draft significantly, but eventually came to consensus as amended and passed. In summary, the bill takes the NDC Program as a standalone quasi-governmental agency, and makes it a program under the direction of the Nevada Department of Administration while continuing to maintain the governance authority with the NDC Committee appointed by the Governor of the State of Nevada. Additionally, the bill establishes and clarifies that the NDC Committee shall act as the Chief of the using agency for the purposes of the Purchasing statute, NRS333.335, and provides clear process and authority of how Requests for Proposals (RFP) will be executed and carried out. Finally, the bill also establishes the ability of the Governor to allow for an individual to be appointed to the NDC Committee that represents a participating political subdivision within the Program. Mid-cap fund reminder As announced earlier in the year, the NDC Committee took action at the February 23, 2017 quarterly committee meeting to add the Vanguard Mid-Cap Value Index Fund (VMVAX) to the NDC Program’s core investment lineup. This passively managed index fund, which became available May 15, provides another investment diversification opportunity at minimal cost to participants. For the fund fact sheet, go to nevada.beready2retire.com. Mark your calendars now During National Retirement Security Week October 9-13, 2017, the NDC Program will host the 11th Annual Financial Wellness Days. Be sure to mark your calendars. Workshops will be held throughout the State of Nevada. More details will be sent out to employees and participants in the months to come and will be published in the next issue of The Deferred Word. In closing, all of us here at NDC wish you and your family a safe and enjoyable summer. |

| NEW TO THE PLAN | ^ top of page |

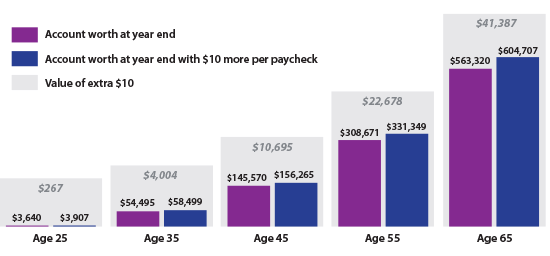

The difference $10 could make Any time you receive a merit step increase or cost-of-living adjustment (COLA) to your salary, consider using that extra money to save more for your retirement. Every dollar you contribute to your NDC account matters. Even a small increase adds Here’s a hypothetical example of what a difference $10 could make. At age 25, Sophia begins participating in the NDC Program. She has $136.11 deducted pre-tax from each biweekly paycheck through age 64. Assuming a 6 percent rate of return, her potential account balance could be $563,320 when she retires at age 65. By saving $10 more per paycheck, she could have a potential account balance of $604,707, a difference of $41,387 more for her retirement.

The year-end value assumes a 6 percent rate of return. This scenario compares cumulative retirement savings between $136.11 and $146.11 per pay period contributions beginning at age 25 through age 64 and no salary increases. This hypothetical illustration is not guaranteed and is not intended to reflect the performance of any specific investment. There is no assurance that increasing contributions will generate investment success. Additionally, these figures do not reflect taxes or any fees or charges that may be assessed by the investments. Systematic investing does not ensure a profit or guarantee against loss in declining markets. Investors should consider their ability to continue investing consistently in up as well as down markets. If you can afford to contribute more, think about doing it today. To change your contribution amount, download and complete the Payroll Contribution Form and fax it to the NDC office at 775-684-3399. Neither the Nevada Deferred Compensation Administration nor the Voya® family of companies offers financial, legal or tax advice. For such advice, consult with a financial or tax advisor or legal attorney.

|

|

| ACTIVELY PARTICIPATING IN THE PLAN | ^ top of page |

How’s your investment mix? Many experts say you should choose a mix of investments for your retirement savings. But do you know why? Keeping too much of the money in your NDC Program account in options that invest in just one particular asset class — stocks, bonds or cash equivalents — could increase risk. For example, a portfolio with only conservative investments may expose you to the risk of outliving your assets. With a portfolio that’s too aggressively invested for growth, the value of your investments might decline sharply just at the moment you need income in retirement. As you invest for retirement, it’s important to remember:

Once you accept that risk is a normal part of investing, you may feel more confident that Diversification involves spreading your account balance among investments in more than one asset class and owning different types of investments within an asset class. Asset allocation is deciding what percentage to invest in an asset class and how to divide it within an asset class. Having a mix of asset classes may help manage risk by increasing the possibility that at least one asset class is performing if others are not. Strong returns in one asset class could also help offset weak performance in another. In fact, broad diversification could potentially enhance your portfolio’s total return without adding more risk. Of course, diversification and asset allocation cannot guarantee a profit or protect against loss in declining markets. However, both strategies could help you balance out the various risks you take as you aim for better returns. The asset allocation you think is right for you will be based on your objectives, how you feel about market volatility, and the amount of time left for investing before you start using the assets in retirement. You can learn more about diversifying the investments in your NDC Program account by visiting nevada.beready2retire.com or by calling 775-886-2400.

|

|

| NEARING RETIREMENT | ^ top of page |

Get your estate in order Estate planning isn’t just for the wealthy. It’s for anyone with an estate. An estate includes all the things of value that you own: bank accounts, life insurance and retirement plan assets, cars, homes, furniture and jewelry, for example. Estate planning spells out exactly how you wish to:

As part of your estate planning, consider creating a living will and/or healthcare proxy that appoints someone to make decisions about your medical care if you become unable to make decisions yourself. A durable power of attorney permits someone you appoint to make financial decisions on your behalf. Many people assume that their assets will automatically get passed on to their spouse, children or other family members. Not necessarily. If there’s no will, a probate court might decide who gets your assets. A will communicates exactly how you want your estate settled. Keep in mind that your will doesn’t override the beneficiary designations on record for a life insurance policy, annuity, or retirement accounts, such as your NDC account and other retirement plan accounts. That means regardless of your current relationship status or what your current will says, the life insurance policy, annuity or retirement account will go to the individuals you named in the beneficiary designations whenever you last updated them. By drafting a will and updating the beneficiaries on your accounts, you’ll take your first steps toward getting your estate in order. Consider meeting with an estate planning advisor and/or attorney about creating and executing vital estate plan documents. Neither the Nevada Deferred Compensation Administration nor the Voya® family of companies offers financial, legal or tax advice. For such advice, consult with a financial or tax advisor or legal attorney.

|

|

| ENJOYING RETIREMENT | ^ top of page |

Using your savings for retirement income During retirement, you have the flexibility to take payments as needed or request scheduled automatic payments from your NDC account. With the NDC Program, you pay no withdrawal fees. As long as there is a balance in your account, you can change your withdrawal option any time, unless you elected an annuity payment option. You may:

It’s important to have a plan for taking withdrawals, both to manage your tax bill and provide for your future income needs. You’ll want to consider the tax consequences of different withdrawal options, perhaps with help from a qualified tax or financial adviser. The amount of federal and state income taxes (if applicable) withheld from your before-tax deferral NDC account and withdrawals and earnings from your Roth 457 account that are not considered a qualified distribution will depend on which withdrawal option you select. Remember, you don’t have to take withdrawals from your NDC account until April 1 following the year in which you reach age 70½ or quit working, whichever happens later. At that point, you will need to begin taking annual RMDs required by the IRS. Whenever you want to start or change your withdrawal option, please call 866-464-6832 or the local Voya® office at 775-886-2400. A representative assigned to the NDC Program by our contracted record keeper, Voya Financial®, will help you understand your choices and complete your request. Neither the Nevada Deferred Compensation Administration nor the Voya® family of companies offers financial, legal or tax advice. For such advice, consult with a financial or tax advisor or legal attorney. |

|

Nevada Public Employees’ Deferred Compensation Program (NDC) Phone 775-684-3397 | Fax 775-684-3399 | defcomp.nv.gov

Securities and investment advisory services offered through Voya Financial Advisors, Inc. (member SIPC) Insurance products, annuities and funding agreements are issued by Voya Retirement Insurance and Annuity Company (“VRIAC”), Windsor, CT. VRIAC is solely responsible for its own financial condition and contractual obligations. Plan administrative services provided by VRIAC or Voya Institutional Plan Services LLC (“VIPS”). VIPS does not engage in the sale or solicitation of securities. All companies are members of the Voya® family of companies. Securities distributed by Voya Financial Partners LLC (member SIPC) or third parties with which it has a selling agreement. All products and services may not be available in all states. Nevada Deferred Compensation is not affiliated with the Voya family of companies. CN0518-34508-0619D

|

|

NEWSLETTER ARCHIVE |

^ top of page |

| 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | |

| • 1st Quarter 17 | • 4th Quarter 16 • 3rd Quarter 16 • 2nd Quarter 16 • 1st Quarter 16 |

• 4th Quarter 15 • 3rd Quarter 15 • 2nd Quarter 15 • 1st Quarter 15 |

• 4th Quarter 14 • Summer 14 • Spring 14 • Winter 14 |

• Fall 13 • Summer 13 • Winter 13 |

• Fall 12 • Spring 12 |

• Fall 11 • Summer 11 • Spring 11 • Winter 11 |

|