|

|||||

| New to the Plan | Actively Participating | Nearing Retirement | Enjoying Retirement | Archives | |

As the fall season begins, the Nevada Public Employees’ Deferred Compensation Program (NDC) prepares for exciting changes and new educational opportunities to assist participants and employees with their Journey to and through retirement. Financial Wellness Days in October Each fall, the NDC Program organizes and hosts workshops in an effort to participate with National Retirement Security Week (NRSW). This year, we invite all government employees and their families to participate in financial wellness workshops during the State of Nevada’s 11th annual Financial Wellness Days October 10 – 13, 2017. MARK YOUR CALENDARS NOW. We have an amazing campaign planned this year. The financial wellness workshop topics will include: Understanding your Public Employee Pension (PERS), Nevada Deferred Compensation Basics and Your Pre-Retirement Checklist, Simplifying Investment Concepts, Investment Management and Advice, Estate Planning and Preservation, Understanding Your Social Security and Medicare Benefits, Preparing For Healthcare Costs Now and Into Retirement and Understanding College Savings Plans in Nevada. Special note: Social Security Administration (SSA) will be presenting on all days. On October 11 at 9 a.m., SSA Rep. Barbara Duckett will be presenting in Las Vegas at the Grant Sawyer Building and video conferencing to a live audience in Carson City at the State Legislative Building for an interactive presentation. Employees are encouraged to attend the SSA Presentation live at both locations this day if they desire. Mrs. Duckett will again be presenting live in Las Vegas along with all of the other presenters on October 12 for a full day of workshops. Attend any workshops you wish. There is no need to register. Workshops will be held live at all locations and broadcast over the Internet on the Carson City and Las Vegas days. Be sure to receive agency approval and sign in at the workshop in order to be paid administrative leave. NAC 284.589. Administrative leave with pay (NRS 284.065, 284.155, 284.345, 284.383, 284.385, 284.390): 1. An appointing authority may grant administrative leave with pay to an employee (f) To attend a general employee-benefits orientation or an educational session relating to employee benefits, including, without limitation, retirement and deferred compensation. Financial Wellness Workshops Schedule Full days of workshops will be 9 a.m.–4 p.m., with a lunch break 12–1 p.m. The Special Social Security Presentation in Las Vegas will be 9–10 a.m.

|

| IMPORTANT PLAN NEWS |

Changes and enhancements to the NDC fee structure As a part of an ongoing process, the NDC Committee and Administration are constantly looking for ways to improve and enhance the value of the NDC Program. To ensure that the NDC Plan remains an effective way for public employees to save and plan for retirement, the NDC Committee regularly reviews the Plan’s investment options, plan fees, and the overall plan design. As our Plan has grown, so too has our ability to reduce the fees our participants pay. By simplifying our investment options, we are able to leverage our plan growth to reduce the fees for our Plan’s investment options. Beginning in December 2017, your investments and ongoing contributions will be directed to a new investment and fee structure. This mapping will be based on your allocation on record with our contracted recordkeeper, Voya Financial®, as of the close of the New York Stock Exchange (NYSE), generally 1:00 p.m. Pacific Time, on December 21, 2017. These changes will take place automatically. You are not required to do anything. What’s not changing:

What is changing: Consistent with the Plan’s goals of fee transparency and cost equitability, effective December 21, 2017, the fee structure will change how the Plan’s costs are paid by participants. The new fee structure will consist of two parts:

Please contact the NDC Administrative Office for further information. NDC’s Administrative staff, Voya’s representatives and dedicated staff are available by phone or appointment to provide you additional information, answer your questions or address any concerns you may have.

|

| NEW TO THE PLAN | ^ top of page | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Understanding your investment options With the NDC Program, you decide how to invest the money in your account. So whether you want someone else to manage your investments or prefer to do it yourself, there are different funds to help meet your needs. Target retirement date funds Target retirement date funds offer a convenient approach if you do not have the time, knowledge, interest and/or experience to select and actively manage your retirement portfolio. With a target retirement date fund, you choose the fund with the target date when you anticipate retiring, and the fund manager handles the rest. Over time, as the target date approaches, the fund goes from being more aggressive to becoming more conservative, with the fund manager decreasing the exposure to aggressive stocks and increasing exposure to more conservative assets like bonds or more stable value type investments. It is important to understand that even with a target retirement date fund (as with all market securities), principal value is never guaranteed (even when the target date is reached), and there is no guarantee that the fund will provide adequate retirement income to meet an investor’s objectives. Remember, as with any market security, it is possible to lose money, including losses near or in retirement. A wide menu of funds If you feel comfortable with investing, you may customize your retirement portfolio based on your objectives and the type of investor you are. Funds are available in the major asset classes (stocks, bonds and cash equivalents), from most conservative to aggressive: stability of principal, bonds, balanced, large cap growth and value stocks, small/mid/specialty stocks and global/international stocks. The funds’ investment objectives, strategies and potential risks and returns vary. Please feel free to reach out to any of the representatives from the NDC contracted record keeper, Voya Financial®, for one-on-one education about the NDC Program’s investment options. Fund fact sheets are available at nevada.beready2retire.com or by calling 866-464-6832. You should consider the investment objectives, risks and charges and expenses of the investment options offered through the plan carefully before investing. The fund prospectuses and information booklet containing this and other information can be obtained by contacting your local representative. Please read the information carefully before investing.

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ACTIVELY PARTICIPATING IN THE PLAN | ^ top of page | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

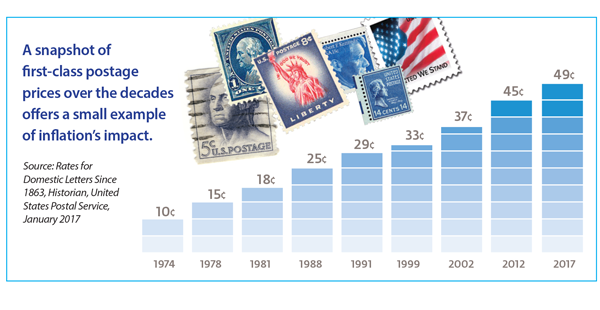

How inflation affects retirement The reality of inflation is important to think about as you plan and invest for your retirement. Inflation refers to the increase in the price of any good or service. Prices tend to rise over time. The rate of inflation has averaged about 3% in the years since 1979 when the rate peaked at 13.3%.1 That may not seem threatening — until you consider its long-term impact. For example, 3% annual inflation would increase the price of a car that costs $20,000 today to almost $27,000 just 10 years from now. In 24 years, you’d need twice as much money as you spend today to maintain your current standard of living. As you can see, the purchasing power of your retirement savings is likely to go down as time goes by. There are some steps you can take now to help protect yourself against the corrosive effect of inflation.

1 Bureau of Labor Statistics, “Consumer Price Index for All Urban Consumers Historical Tables, 1913 to the Present.”

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NEARING RETIREMENT | ^ top of page | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

What type of investor are you? Understanding what type of investor you are helps you set and follow the investment strategy right for you. To help you do this, the NDC Program gives you access to a self-assessment questionnaire. Your responses help identify your tolerance for risk, your investor profile and a model portfolio with sample allocations for each asset class. Check the box that matches your answer to each question.

If your investor profile is close to what you expected, and the asset allocation of your NDC account’s investments matches your profile, good for you! But if your investor profile surprises you, it may be time to take action, especially since you’re closer to retiring and have a shorter investing timeline. Consider using these questions to start a conversation about your situation with your financial advisor. Neither the Nevada Deferred Compensation Administration nor the Voya® family of companies offers tax or legal advice. For such advice, consult with a tax or legal advisor.

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ENJOYING RETIREMENT | ^ top of page | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

Are you age 70½ or older? Federal income tax laws say that once you reach age 70½ and have left employment with the State of Nevada, you will need to begin withdrawing at least a minimum amount, known as a Required Minimum Distribution (RMD), from your NDC account and other retirement plan accounts annually. You can always withdraw more than the required minimum amount in any year. But if you don’t make your annual minimum taxable withdrawals, you could be subject to a 50 percent penalty tax payable to the Internal Revenue Service on the amount that should have been withdrawn by the deadline. Deadlines. Your first required minimum distribution must be taken by April 1 in the year after the year in which you turn 70½ or when you stop working, whichever is later. After your first RMD, your next withdrawal must be taken each year by December 31. If you delay taking your first RMD until April 1 of the year following the year you reach age 70½, you will be required to take two distributions during that calendar year and both payments will be taxable in the same year. If you don’t want to take two withdrawals in the same year, you can request that your first withdrawal be taken in December of the year you turn age 70½. Amounts. Your RMDs will vary based on your life expectancy. Generally, your payment will be calculated by dividing your NDC account’s year-end cash value amount of the prior year by the life expectancy factor on the IRS Uniform Lifetime Table. If your spouse is named as your sole primary beneficiary and is more than 10 years younger than you, a joint life expectancy calculation is applied, resulting in a smaller required distribution. Getting started. You will receive a letter from the NDC contracted record keeper, Voya Financial®, that explains the dollar amount and timing of your RMD payment. Your RMD is calculated automatically and information is mailed to you in November of the year you turn 70½. Regular payments. After you take your first RMD, you will receive a letter every November stating the RMD dollar amount that will be withdrawn from your NDC account and paid to you in December. Retirement plan distributions are considered ordinary income on which taxes must be paid and will be reported on IRS Form 1099R. Voya Financial® will automatically withhold 10% federal tax. You have the choice of additional withholdings if necessary. Neither the Nevada Deferred Compensation Administration nor the Voya® family of companies offers financial, legal or tax advice. For such advice, consult with a financial or tax advisor or legal attorney. |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||

Nevada Public Employees’ Deferred Compensation Program (NDC) Phone 775-684-3397 | Fax 775-684-3399 | defcomp.nv.gov

Securities and investment advisory services offered through Voya Financial Advisors, Inc. (member SIPC) Insurance products, annuities and funding agreements are issued by Voya Retirement Insurance and Annuity Company (“VRIAC”), Windsor, CT. VRIAC is solely responsible for its own financial condition and contractual obligations. Plan administrative services provided by VRIAC or Voya Institutional Plan Services LLC (“VIPS”). VIPS does not engage in the sale or solicitation of securities. All companies are members of the Voya® family of companies. Securities distributed by Voya Financial Partners LLC (member SIPC) or third parties with which it has a selling agreement. All products and services may not be available in all states. Nevada Deferred Compensation is not affiliated with the Voya family of companies. CN0815-36509-0919D

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

NEWSLETTER ARCHIVE |

^ top of page |

| 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | |

| • 2nd Quarter 17 • 1st Quarter 17 |

• 4th Quarter 16 • 3rd Quarter 16 • 2nd Quarter 16 • 1st Quarter 16 |

• 4th Quarter 15 • 3rd Quarter 15 • 2nd Quarter 15 • 1st Quarter 15 |

• 4th Quarter 14 • Summer 14 • Spring 14 • Winter 14 |

• Fall 13 • Summer 13 • Winter 13 |

• Fall 12 • Spring 12 |

• Fall 11 • Summer 11 • Spring 11 • Winter 11 |

|