|

|||||

| New to the Plan | Actively Participating | Nearing Retirement | Enjoying Retirement | Archives | |

What's New With 2020 off and running, and the first quarter of the year bringing economic and health crisis challenges, most Nevadans are excited to bring in the Spring and Summer months. NDC continues working hard to bring the most value to participants, and develop and sponsor many exciting educational opportunities to assist employees with their Journey to and Through Retirement. Retirement Reform — SECURE Act and CARES Act: What’s on the Horizon? With the passage of the SECURE Act in December 2019, and the passage and implementation of the CARES Act stimulus near the end of the first quarter of 2020, the NDC Committee is evaluating what effects these two pieces of legislation may or may not have on Program management. This includes choosing to elect to adopt some or all of optional provisions included in the legislation. In the upcoming months, the NDC Committee and Administration will be evaluating what provisions, if any, we may consider amending into our current Plan design. Items we will be considering are:

Mandatory changes that have been implemented as a result of the passage of the SECURE Act is that the Required Minimum Distribution (RMD) age has changed from 70½ to 72 years of age. With the passage of the CARES Act, the RMD requirement for 2020 has been waived for those that have not already distributed their RMD for the 2020 calendar tax year. As fiduciaries to the Plan and prior to implementing optional changes, NDC will always analyze what is going to be in the collective best interest of participants in the Program with the goal of attempting to benefit 100% of participants. If the NDC Administration elects to make changes or enhancements to the Program, we will work quickly to communicate the changes to our participant and eligible employee base. Investment Consultant Services RFP Completed The NDC Administration and State Purchasing Division have concluded the Plan’s Investment Consulting Services Request for Proposal (RFP) solicitation. An Evaluation Committee organized by State Purchasing evaluated proposals from five different vendors that met the minimum qualification criteria in the solicitation, and the Hyas Group was the highest scoring vendor. The NDC Committee took action to direct the Executive Officer and State Purchasing to begin contract negotiations with Hyas. Negotiations were successful and a contract has been executed. This contract is slated to be heard and approved on the May 14th BOE meeting, with a June 1, 2020 contract start date. In closing, all of us here at NDC wish you and your family a safe and enjoyable Spring Season.

|

| NEW TO THE PLAN | ^ top of page | ||||||||||||||||||

Pay Student Loan Debt or Save for Retirement? Paying student loan debt? Paying down student debt first before you start saving for the future may be the most helpful because it could help reduce stress, but remember that all loans are not created equal. Most federal loans have lower interest rates, meaning it won’t cost you as much in interest to take longer to pay off your loans, which means you can start saving for retirement sooner. If you have a higher interest rate personal student loan, it may make sense to pay this down faster and make smaller contributions to your retirement plan in the meantime.¹ What about saving for retirement? The sooner you can save, the longer you can take advantage of potential compounding interest on savings that can help add up over time. Saving pre-tax money impacts your net pay by less than you think. For example, saving $50 pre-tax per paycheck to your NDC account impacts your net paycheck by only $36.2 The bottom line is, getting an education was an important investment in yourself and loans from it are often just a part of life. But so is saving for retirement, even if it’s just a little bit now. Whatever you do, we want you to feel good about your money, your life, and your future. Sources: ¹Should I pay off student loans or save for retirement, Maurie Backman, June 24, 2019, Motley Fool, The Ascent 2Assumes savings are made in a pre-tax account at a 28% tax rate. This hypothetical example is not guaranteed and does not reflect any specific product. Investments are subject to investment risk including the possible loss of principal. The investment return and principal value of the security will fluctuate so that when redeemed, may be worth more of less than the original investment. In addition, these figures do not reflect taxes or any fees, expenses or charges of any investment product.

|

|

||||||||||||||||||

| ACTIVELY PARTICIPATING IN THE PLAN | ^ top of page | ||||||||||||||||||

As the markets change, the value of each security in your NDC portfolio will increase or decrease at a different rate of return and change the overall weightings of your investments. The result is asset allocations that may no longer match your risk or long-term goals. It may be time to rebalance your account. Periodic review and rebalancing of your investment portfolio can help keep your retirement strategy on track. Rebalancing in your NDC account means adjusting your individual investment holdings—that is, buying and selling stock and bond funds within the NDC investment lineup—to maintain your established asset allocation percentages and remain consistent. Finding that balance helps maintain your original allocation while keeping your tolerance for risk at its most comfortable level. Whether there is market volatility or not, it’s a good idea to review the value of your investments regularly so you can know if you need to rebalance at all. This will help you stay balanced and stomach the changes that may occur on your journey to retirement. Your NDC Plan offers auto rebalancing within your account as well, which could help you find your balance and sense of well-being while investing. If you gain asset value, it’s great. Increases to your investments, however, move your portfolio allocations away from your original strategy. You may find for example, your portfolio is now weighted more heavily in stocks, which may expose you to more risk than intended. One-time or regularly scheduled automatic rebalancing at a frequency you elect helps redistribute the weight and keep your stock and bond assets properly allocated within your portfolio. Remember, rebalancing doesn’t ensure a profit or protect against a loss in a declining market, but it will help you stick to a strategy that you believe is appropriate for you when markets shift or if your goals change so you can retire well.

|

|

||||||||||||||||||

NEARING RETIREMENT |

^ top of page | ||||||||||||||||||

Stick to the plan when markets correct – it’s normal Stock market growth is great for your retirement savings, but history tells us that it can’t last forever. Market “correction” could happen at any time, but the potential for gains or losses should always be expected as a part of investing. So how do you manage your expectations? Here are some things to keep in mind amid times of uncertainty:

While it’s important to be aware of what the market is doing, keep in mind that fluctuation is normal and should be expected. Sticking to your plan and your long-term goals can help you stay on course as you work toward your retirement objectives. The Penalty for Missing the Market Trying to time the market can be an inexact – and costly – excercise.* This chart illustrates a return on a lump sum investment of $10,000 invested in the S&P 500 Index from January 22, 1985 to January 21, 2015.

Past performance is no guarantee of future results. Performance shown is historical index performance and not illustrative of any specific funds’ Performance. This is a hypothetical example used for illustrative purposes only. The return figures are based on a hypothetical $10,000 investment in the S&P 500 Index from January 22, 1985 - January 21, 2015. The lump sum investment in common stocks would have reflected the same stocks/weightings as represented in the S&P 500 Index. The example does not represent or project the actual performance of any security, or other investment product. The hypothetical figures do not reflect the impact of any commissions, fees or taxes applicable to an actual investment. The S&P 500®Index is an unmanaged, market capitalization-weighted index of 500 widely held U.S. stocks recognized by investors to be representative of the stock market in general. It is provided to represent the investment environment existing for the time period shown. The returns shown do not reflect the actual cost of investing in the instruments that comprise it. You cannot invest in an index. Standard & Poor’s and S&P 500 are trademarks of the McGraw-Hill Companies, Inc. *Source: Commodity Systems, Inc. (CSI) via Yahoo Finance

|

|

||||||||||||||||||

| ENJOYING RETIREMENT | ^ top of page | ||||||||||||||||||

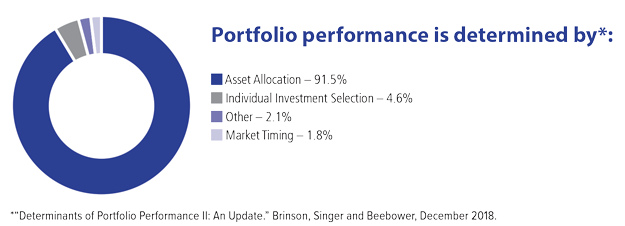

Simplifying investment concepts Unless you’re a financial professional, financial terms can be confusing to understand. Take asset allocation and diversification, for example. While they are often used together when investing, they are distinct and different. What is asset allocation?

What is diversification?

Asset allocation and diversification neither assures nor guarantees better performance and cannot protect against loss in declining markets or better performance, but it is a well-recognized risk management strategy. Still not sure? A financial professional can review your investment strategy to help make a plan that is right for you. Remember, it’s never too late to get your financial life in order.

|

|

||||||||||||||||||

| ^ top of page | |||||||||||||||||||

Actions you can take to help you navigate today and keep saving for tomorrow Feeling anxious and unsure about the future? The world has proven to be unpredictable the last few weeks and even though many of us may be worried about the short-term, it’s important to not lose sight of your future. Here are some suggestions and resources to help you navigate today’s uncertainty and plan for your tomorrow.

|

|||||||||||||||||||

Nevada Public Employees’ Deferred Compensation Program (NDC) Phone 775-684-3397 | Fax 775-684-3399 | defcomp.nv.gov

This information is provided by Voya for your education only. Neither Voya nor its representatives offer tax or legal advice. Please consult your tax or legal advisor before making a tax-related investment/insurance decision. Insurance products, annuities and funding agreements are issued by Voya Retirement Insurance and Annuity Company (“VRIAC”), Windsor, CT. VRIAC is solely responsible for its own financial condition and contractual obligations. Plan administrative services provided by VRIAC or Voya Institutional Plan Services LLC (“VIPS”). VIPS does not engage in the sale or solicitation of securities. All companies are members of the Voya® family of companies. Securities distributed by Voya Financial Partners LLC (member SIPC) or third parties with which it has a selling agreement. All products and services may not be available in all states. Nevada Deferred Compensation is not affiliated with the Voya family of companies. CN1154674_0422

|

|||||||||||||||||||

NEWSLETTER ARCHIVE |

^ top of page |

| 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | |

| • 1st Quarter 19 • 2nd Quarter 19 • 3rd Quarter 19 • 4th Quarter 19 |

• 1st Quarter 18 • 2nd Quarter 18 • 3rd Quarter 18 • 4th Quarter 18 |

• 4th Quarter 17 • 3rd Quarter 17 • 2nd Quarter 17 • 1st Quarter 17 |

• 4th Quarter 16 • 3rd Quarter 16 • 2nd Quarter 16 • 1st Quarter 16 |

• 4th Quarter 15 • 3rd Quarter 15 • 2nd Quarter 15 • 1st Quarter 15 |

• 4th Quarter 14 • Summer 14 • Spring 14 • Winter 14 |

• Fall 13 • Summer 13 • Winter 13 |

• Fall 12 • Spring 12 |

|